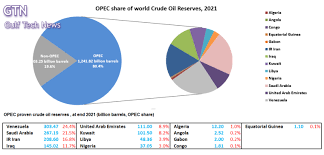

There have been contrasting views on oil by both OPEC+ and the US. The cartel’s concern about a slowing global economy partially motivated its cuts of crude output on Oct 5. The US is worried about supply shortages following Russia’s invasion of Ukraine. Bloomberg estimates show the market is exhibiting both demand weakness and supply scarcity.

The slowing global growth was behind the softness in consumption, with the world’s largest three economies — the US, China and Europe — either heading toward a recession or facing a meaningful slowdown.

Output shortages drove nearly two-thirds of the oil rally between December and June. In this period, the price surged from nearly $70 per barrel to over $120.

Outages began before Russia’s invasion of Ukraine, but the war intensified the problem. Shortage of demand has been responsible for almost three-quarters of the fall in crude prices since June and oil has dropped about $30 in this interval.

Supply shortages have lifted oil prices by $30 since December 2021, taking the price of a barrel to near $90. This has impacted the world’s biggest economies differently. Bloomberg estimates the drag on growth ranges from near zero in the US, to 0.2 percentage point in China, and 0.8 ppt in the euro area. The increase in US oil production and reduced energy intensity of output globally mean the drag from rising prices is smaller than in the past.

Ziad Daoud, Chief Emerging Markets Economist for Bloomberg Economics, outlines the steps to estimate the impact of oil price changes on global growth:

The first step to estimating the impact of oil price moves on global growth is to isolate the contribution of changes in supply (which impact global growth) from moves in demand (a symptom of shifts in global growth).

To do that, we use a sign restriction model based on the co- and contrary-movement of oil and equity prices (more details on that below). The model shows since the December trough, supply shortages have driven a $30 increase in oil prices and weak demand has subtracted $9.

Next, we compute the historical response of GDP growth in the world’s three largest economies to oil supply shocks using data from 2000. Our model allows for responses that can vary over time so we can gauge how the sensitivities have changed.

Our estimates show the drag from oil prices is highest in the euro area and lowest in the US. China is somewhere in between. The effects are consistent with the US switching from a net importer of oil and liquid fuel to a net exporter in the 2010s.

The model also shows global growth has become less sensitive to oil over the last two decades. The impact has fallen by three quarters in the US and nearly half in China and the euro area. Energy efficiency has helped — the number of oil barrels needed to produce one unit of global GDP has dropped by nearly 40% since 2000.

Two caveats: first, the shale oil revolution that benefited the US in the 2010s may not help the economy today. The industry is focusing on profitability rather than expanding output. This means the drag on US growth from higher oil prices may be greater today than our 2019 estimate.

Second, even with a low impact on growth, there are distributional effects to higher oil prices in the US. Higher prices bump up the profits of a small base of energy producers, but lower the purchasing power of a large number of consumers.