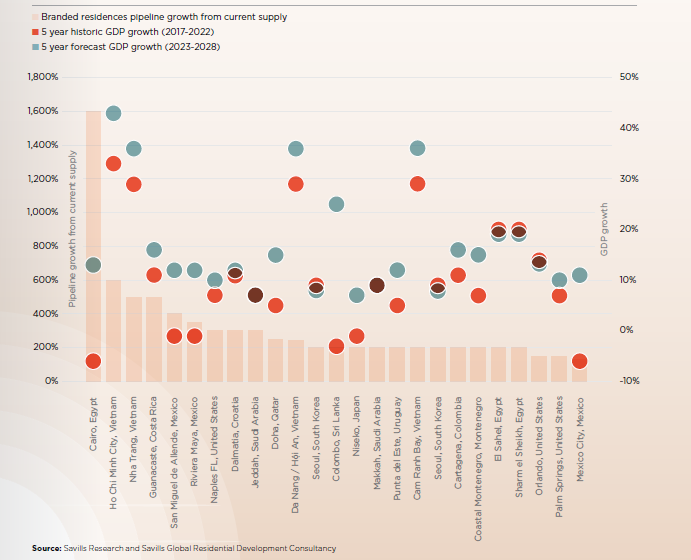

The highest growth over the pipeline period until 2030 can be found in the Middle East

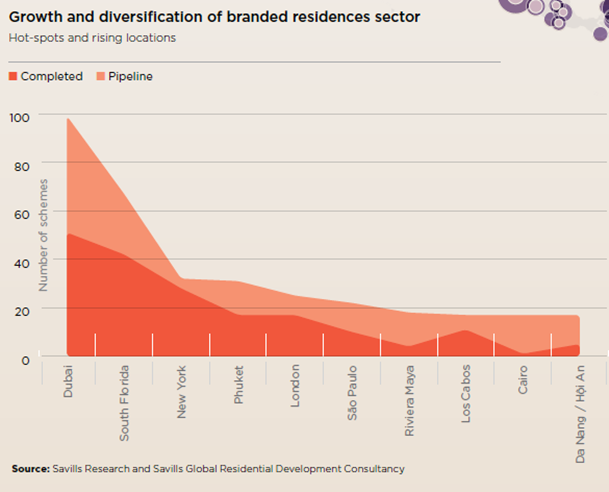

By a considerable measure, the hottest of hotspots for branded residences is Dubai, with 51 operational schemes, property consultancy Savills said in its latest Branded Residences Report.

The total supply of branded residences in the city is expected to nearly double by the end of the forecast period until 2030. A close second in terms of completed schemes is South Florida, with 42 completed schemes.

“These two markets each appeal to international buyers, especially those seeking trophy assets, and have witnessed significant economic growth in recent years,” says Kelcie Sellers, associate, Savills World Research.

Branded residences as a sector have remained resilient in the face of global headwinds. The number of branded residences schemes has increased by over 160% in the last decade, with new brands, locations, and a shift in amenities set to propel the sector even further. With more than 690 completed schemes globally, a further 600 are expected to be delivered by 2030, says Savills.

“Once accounting for all of the schemes in existence, today North America accounts for just over one-third of the total supply. In the past 30 years, as the sector has grown, it has expanded into all regions; Asia Pacific and the Middle East are hotspots as they are home to an additional 40% of total supply,” explains Sellers.

The highest growth over the pipeline period can be found in the Middle East (+120%) and in Central and Latin America (+89%), with all global regions forecast to exhibit high levels of growth to 2030.

Over the coming years, branded residences are set to continue their growth world-wide, with substantial growth anticipated in emerging cities. Cairo, for example, is forecast to see the highest pipeline growth moving from one operational scheme to 17 by the end of 2030. Ho Chi Minh City, Nha Trang, Guanacaste, and San Miguel de Allende complete the top five, each with forecast growth of more than 400% by 2030.

“Demand for luxury branded residences from domestic buyers is likely to grow faster in emerging cities, where the quality of the existing stock is unlikely to meet the requirements of those looking for high-quality fitouts and services. In these markets, there will be opportunities for urban, upper-upscale residences as well as luxury products for brand-loyal, well-travelled customers,” said Sellers.

When it comes to market leaders, Marriott International remains in first place, a position it has held since 2002, followed by Accor and Four Seasons. In terms of the hotel brands themselves, Four Seasons, The Ritz-Carlton, and St. Regis lead the space (the latter two within the Marriott International portfolio of brands). Non-US parent companies such as Emaar Hospitality and Banyan Tree Group have risen to become global contenders. Despite the space being dominated by hotels, Savills estimates that non-hotel brands will account for 20% of the total supply by 2030, an increase of approximately 40% from current levels.

Within hotel brands, whilst luxury chains still account for two-thirds of completed schemes, upper-upscale and upscale brands are increasing their presence and are forecast to increase their market share by 50% and 70%, respectively.

“Branded residences have diversified from being entirely luxury hotel-driven to offering products across all hotel chain scales. We are also witnessing an influx of non-hotel brands from a wide range of sectors including the fashion, design, and automotive spaces. New brands set to enter the sector include Dolce & Gabbana, De Grisogono, Mama Shelter, and Rare Finds,” says Rico Picenoni, head of Savills Global Residential Development Consultancy.

In terms of non-hotel brands, YOO remains in the top spot, however brands such as Pininfarina (Mahindra), Elie Saab, and Versace (Capri Holdings) are set to move up the rankings over the coming years.